WMHW Alert: SEC Amends Enforcement Manual for the First Time Since 2017, Reflecting the Atkins Era Regulatory Shift

March 05, 2026

In The News

WMHW Alert: SEC Amends Enforcement Manual for the First Time Since 2017, Reflecting the Atkins Era Regulatory Shift

March 5, 2026

By Barry Rashkover and Sarah G. DeYoung

For the first time since 2017, the Securities and Exchange Commission (“SEC” or “Commission”) has updated its Enforcement Manual.[1] Published on February 24, 2026, the 2026 Manual serves as the primary reference guide for the Division of Enforcement staff.[2] The 2026 Manual is not merely a housekeeping update; it reflects the significant enforcement shifts observed under the leadership of Chairman Paul Atkins.[3] Although a careful review of the 2026 Manual against the 2017 Manual reveals dozens of changes, this Alert discusses – and summarizes in the chart below – the key changes reflecting the policy shift, as well as important updates modernizing and standardizing aspects of SEC enforcement processes.

Updates Memorializing Policy Goals and Implementing New Laws

The 2026 Manual incorporates several policy shifts that Walden Macht Haran & Williams has tracked over the past year,[4] as well as Executive Order 14294, which disfavors criminal enforcement of regulatory offenses,[5] and the National Defense Authorization Act for Fiscal Year 2021 (“NDAA”), which sets the statute of limitations regarding SEC enforcement actions.[6]

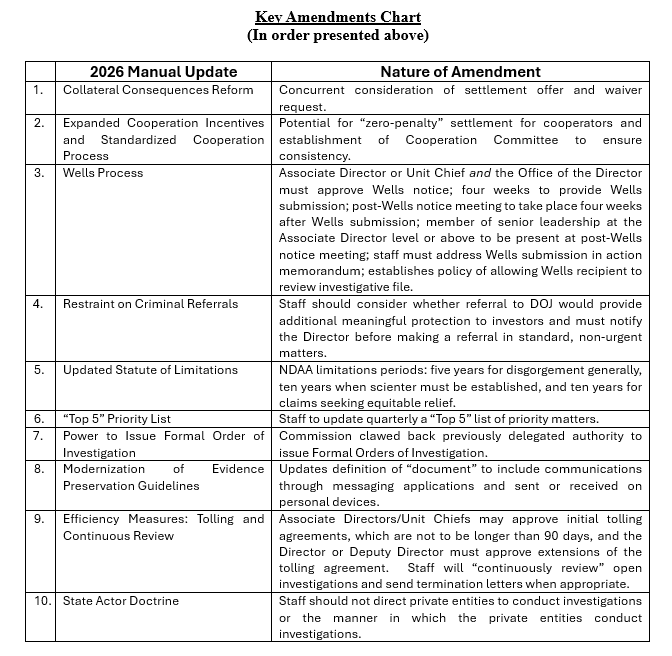

- Reform of Collateral Consequences

Perhaps most significantly, the 2026 Manual sets forth reforms to improve the process for seeking Commission waivers of collateral consequences arising out of SEC enforcement actions. The 2026 Manual incorporates Chairman Atkins’ September 2025 pronouncement that the SEC would restore its prior practice of permitting a settling party to request that the Commission simultaneously consider an offer of settlement and waivers from automatic disqualifications and other collateral consequences, and back out of the settlement should the Commission accept the settlement but deny the requested waivers.[7] This process helps eliminate some of the uncertainty that previously plagued settling parties regarding the full scope of a resolution’s impact. This is an important first step to improving the collateral consequence waiver process – a process that remains critical given that some collateral consequences, such as the bad actor disqualification and Investment Company Act of 1940 Section 9(a) bar, often can be more impactful for a settling party than the SEC enforcement remedies in the settlement itself.

- Expanded Cooperation Incentives: the “Zero Penalty” Settlement

The 2026 Manual expands the framework for cooperation, explicitly describing the possibility of a “zero-penalty settlement” for cooperators and establishing a Cooperation Committee to ensure that cooperation decisions are consistent.[8] The 2026 Manual memorializes and expands upon the criteria to determine cooperation outlined in the Seaboard Report by, for example, enumerating examples of effective remediation and exemplary cooperation.[9] These reforms are aligned with Chairman Atkins’ remarks during his first tenure that companies “should have a clear understanding of what it takes to receive cooperation credit” and that such credit “should be fairly and evenly distributed.”[10]

- Standardization of the Wells Process

The 2026 Manual memorializes the changes to the Wells process that Chairman Atkins announced and that Director of Enforcement Judge Margaret Ryan reaffirmed.[11] The 2026 Manual provides that the issuance of a Wells notice requires approval from the Associate Director or Unit Chief and the Office of the Director, a standardized four-week timeline for recipients to provide a Wells submission, a standardized four-week timeline for the post-Wells notice meeting to occur after receipt of the Wells submission, and that the post-Wells notice meeting must include a member of senior leadership at the Associate Director level or above.[12] The 2026 Manual gives related guidelines for the staff’s action memorandum recommending enforcement: it should “objectively address[] significant evidentiary issues, litigation risks, and the primary arguments in any Wells submissions and White Papers that were accepted,” as well as detail if any Wells notices were provided or explain why they were not provided, and explain why any Wells submissions or White Papers were rejected.[13] Consistent with Chairman Atkins’ comments in October,[14] during the Wells process, the staff “should be forthcoming about the content of the investigative file,” and on a case-by-case basis “should make reasonable efforts to allow the recipient of the Wells notice to review relevant portions of the investigative file.”[15]

- Restraint on Criminal Referrals

The 2026 Manual incorporates the Criminal Referral Policy Statement issued in June 2025 pursuant to Executive Order 14294.[16] Section 5.6.1 now requires staff to consider specific factors before referring conduct to the Department of Justice, including whether the involvement of criminal authorities would provide “additional meaningful protection to investors.”[17] Further, the 2026 Manual implements a specific procedure for criminal referrals in standard, non-urgent matters: staff must notify the Director of their intention to make a criminal referral, and the Director will respond to the referral request within 48 hours. The 2026 Manual instructs that staff should not make a referral in such matters until they hear from the Director.[18]

- Updated Statute of Limitations

The 2026 Manual reflects the NDAA’s updates to the statute of limitations for aspects of SEC enforcement actions.[19] For disgorgement generally, the limitations period is five years. But that period is extended to ten years for securities law violations where scienter must be established. Additionally, the NDAA provides a ten-year limitations period for claims seeking equitable remedies.[20]

Improving Efficiency and Modernizing Practices

Additional updates provide specific procedures to modernize workflows, centralize authority, or adjust investigative tactics.

- The “Top 5” Priority List. Replacing the concept of “National Priority Matters” designated by the Director of Enforcement, the 2026 Manual requires Associate Directors and Unit Chiefs to explicitly designate and update quarterly a “Top 5” list of priority matters.[21]

- Centralization of Formal Order Authority. Memorializing guidance the SEC issued in early 2025,[22] the Commission has clawed back for itself the authority to issue Formal Orders of Investigation.[23] Staff must submit its formal order memorandum and proposed Formal Order to the Commission for approval, no longer the senior enforcement staff.[24]

- Evidence Preservation. The 2026 Manual modernizes the definition of “document” to include communications via messaging applications (e.g., WhatsApp, iMessage, and Signal) and messages sent or received on personal devices.[25]

- Efficiency Measures: Tolling Agreements and Continuous Review. The 2026 Manual places guardrails on staff’s ability to seek a tolling agreement. First, the 2026 Manual provides that initial agreements not toll the limitations period for longer than 90 days, and be subject to approval by Associate Directors/Unit Chiefs. Second, the Manual requires approval from the Director or Deputy Director to extend tolling agreements beyond the initial 90 days.[26] Staff should “continuously review” the status of open investigations and send termination letters when appropriate, rather than waiting for formal case closure.[27]

- State Actor Doctrine. The 2026 Manual expands the discussion on the State Actor Doctrine to explicitly instruct staff to “not direct the private entity to conduct an investigation or mandate the manner in which the private entity conducts an investigation.” The Manual reminds private entities that undertake investigations that “the staff finds indicia of the investigation’s independence, thoroughness, and effectiveness to be helpful indicators” when deciding to credit the investigation’s findings.[28]

***

The Commission has pledged to review the Enforcement Manual yearly, [29] which is encouraging. Time will tell, however, how this will work, whether it will actually result in an annually updated Manual, and whether this creates an opportunity for defense counsel and others to communicate ongoing suggestions to the SEC enforcement staff. Walden Macht Haran & Williams will continue to monitor these developments.

***

Disclaimer:

These materials contain attorney advertising. Prior results do not guarantee a similar outcome and results depend upon a variety of factors unique to each circumstance. WMHW provides this information as a service to clients and other friends for educational purposes only. It should not be construed or relied on as legal advice, or to create a lawyer-client relationship. Readers should not act upon this information without seeking advice from professional advisers.

[1] U.S. Sec. & Exch. Comm’n, Press Release: SEC’s Division of Enforcement Announces Update to Enforcement Manual, SEC.gov (Feb. 24, 2026), https://www.sec.gov/newsroom/press-releases/2026-20-secs-division-enforcement-announces-updates-enforcement-manual.

[2] U.S. Sec. & Exch. Comm’n, Div. of Enf’t, Enforcement Manual (Feb. 24, 2026), https://www.sec.gov/divisions/enforce/enforcementmanual.pdf [hereinafter 2026 Enforcement Manual].

[3] See generally Barry Rashkover, WMHW Alert: SEC Chair Paul Atkins Signals Regulatory Shift, wmhwlaw.com (May 27, 2025), https://wmhwlaw.com/2025/05/27/wmhw-alert-sec-chair-paul-atkins-signals-regulatory-shift/.

[4] Barry Rashkover & Paul W. Ryan, WMHW Alert: SEC Enforcement Trends in the First Six Months, wmhwlaw.com (Oct. 17, 2025), https://wmhwlaw.com/2025/10/17/wmhw-alert-sec-enforcement-trends-in-the-first-six-months/.

[5] Exec. Order No. 14,294, 90 Fed. Reg. 20363 (May 9, 2025).

[6] 15 U.S.C. § 78u(d)(8).

[7] Paul S. Atkins, Statement on Simultaneous Commission Consideration of Settlement Offers and Related Waiver Requests, SEC.gov (Sept. 26, 2025), https://www.sec.gov/newsroom/speeches-statements/atkins-2025-simultaneous-consideration-settlement; 2026 Enforcement Manual § 2.5.2.1.

[8] 2026 Enforcement Manual §§ 6.1.2, 6.2.1.

[9] Report of Investigation Pursuant to Section 21(a) of the Securities Exchange Act of 1934 and Commission Statement on the Relationship of Cooperation to Agency Enforcement Decisions, Exchange Act Release No. 44969 (Oct. 23, 2001), https://www.sec.gov/litigation/investreport/34-44969.htm; 2026 Enforcement Manual § 6.1.2 (effective remediation includes “[h]iring new financial and accounting staff to address accounting and disclosure issues,” and exemplary cooperation includes “[f]acilitating voluntary interviews of witnesses”).

[10] Paul S. Atkins, Speech by SEC Commissioner: Remarks to the ‘SEC Speaks in 2008’ Program of the Practising Law Institute, SEC.gov (Feb. 8, 2008), https://www.sec.gov/news/speech/2008/spch020808psa.htm.

[11] Paul S. Atkins, Keynote Address at the 25th Annual A.A. Sommer, Jr. Lecture on Corporate, Securities, and Financial Law, SEC.gov (Oct. 7, 2025), https://www.sec.gov/newsroom/speeches-statements/atkins-100925-keynote-address-25th-annual-aa-sommer-jr-lecture-corporate-securities-financial-law (“Going forward, the staff will provide the other side with at least four weeks to make Wells submissions.”); Margaret Ryan, Remarks to the Los Angeles County Bar Association, SEC.gov (Feb. 11, 2026), https://www.sec.gov/newsroom/speeches-statements/margaret-ryan-02-11-26-remarks-los-angeles-county-bar-association?utm_source=securitiesdocket.beehiiv.com&utm_medium=newsletter&utm_campaign=sec-enforcement-director-margaret-ryan-discusses-enforcement-priorities-in-first-public-remarks&_bhlid=da8db365c5e20ec18c634d48d09daab3ca0a5135 (“A member of the enforcement senior leadership team will attend every Wells meeting . . . .”).

[12] 2026 Enforcement Manual § 2.3.

[13] Id. § 2.5.2.

[14] Paul S. Atkins, Keynote Address at the 25th Annual A.A. Sommer, Jr. Lecture on Corporate, Securities, and Financial Law, SEC.gov (Oct. 7, 2025), https://www.sec.gov/newsroom/speeches-statements/atkins-100925-keynote-address-25th-annual-aa-sommer-jr-lecture-corporate-securities-financial-law (“Providing the potential respondent or defendant with information about potential charges and the key evidence that forms the basis of those potential charges is critical to due process, fairness, and transparency.”).

[15] 2026 Enforcement Manual § 2.3.

[16] Exec. Order No. 14,294, 90 Fed. Reg. 20363 (May 9, 2025); Policy Statement Concerning Agency Referrals for Potential Criminal Enforcement, Release No. 34-103277, 90 Fed. Reg. 26203 (June 20, 2025), https://www.federalregister.gov/documents/2025/06/20/2025-11332/policy-statement-concerning-agency-referrals-for-potential-criminal-enforcement.

[17] 2026 Enforcement Manual §5.6.1.

[18] Id.

[19] 15 U.S.C. § 78u(d)(8).

[20] 2026 Enforcement Manual § 3.1.2.

[21] Id. § 2.2.4.

[22] Delegation of Authority to Director of the Division of Enforcement, Release No. 33-11366, 90 Fed. Reg. 12105 (Mar. 14, 2025), https://www.federalregister.gov/documents/2025/03/14/2025-04064/delegation-of-authority-to-director-of-the-division-of-enforcement.

[23] 2026 Enforcement Manual § 2.2.3.

[24] Id. § 2.2.3.1.

[25] Id. § 3.2.7.3 (“The term ‘document’ also includes all electronic communications, such as email, text messages, messages sent via messaging applications (such as WhatsApp, iMessage, or Signal), messages sent on communications platforms (such as Teams, Slack, Discord, or Telegram), and messages sent or received on personal devices such as smartphones or tablets.”).

[26] Id. § 3.1.2.

[27] Id. § 2.6.2.

[28] Id. § 3.1.4.

[29] U.S. Sec. & Exch. Comm’n, Press Release: SEC’s Division of Enforcement Announces Update to Enforcement Manual, SEC.gov (Feb. 24, 2026), https://www.sec.gov/newsroom/press-releases/2026-20-secs-division-enforcement-announces-updates-enforcement-manual.